By P. Glen Smith, J.D., M.Div.

As the Baby Boomer generation continues to age and the population is living longer, the need for long-term care is greater now than ever before. Unfortunately, many older adults are unprepared for the high costs associated with long-term care. With the average nursing home bill running over $90,000 per year, many risk depleting their life savings in just a few short years.

As an increasing number of older adults are faced with this reality, they are searching for guidance and looking for someone to help protect themselves, their loved ones and their hard-earned assets. That’s where Lifescape Law & Development comes in.

COST OF CARE

IN-HOME CARE

Average Cost: $4,576 per month*

- Regular support from a professional caregiver

- Maintain a level of independence in their own home

Ideally, most older adults want to remain at home for as long as possible. While some are able to do so, many others eventually require more hands-on care at an assisted living facility or nursing home.

ASSISTED LIVING FACILITY

Average Cost: $4,300 per month*

- Blend full-time care with a level of autonomy

- Assistance with some daily activities

An assisted living facility is a great option for older people who can no longer live at home but desire to maintain some independence. As they age, however, they may need a higher level of care.

NURSING HOME

Average Cost: $7,756 per month*

- Round-the-clock nursing care and support

- Assistance with Activities of Daily Living (ADLs)

As their health deteriorates and they require more hands-on-support, many older people need nursing home care. Fortunately, we can help them protect their life savings from the high cost. Roughly 60% of residents will transition from assisted living to a skilled nursing facility.

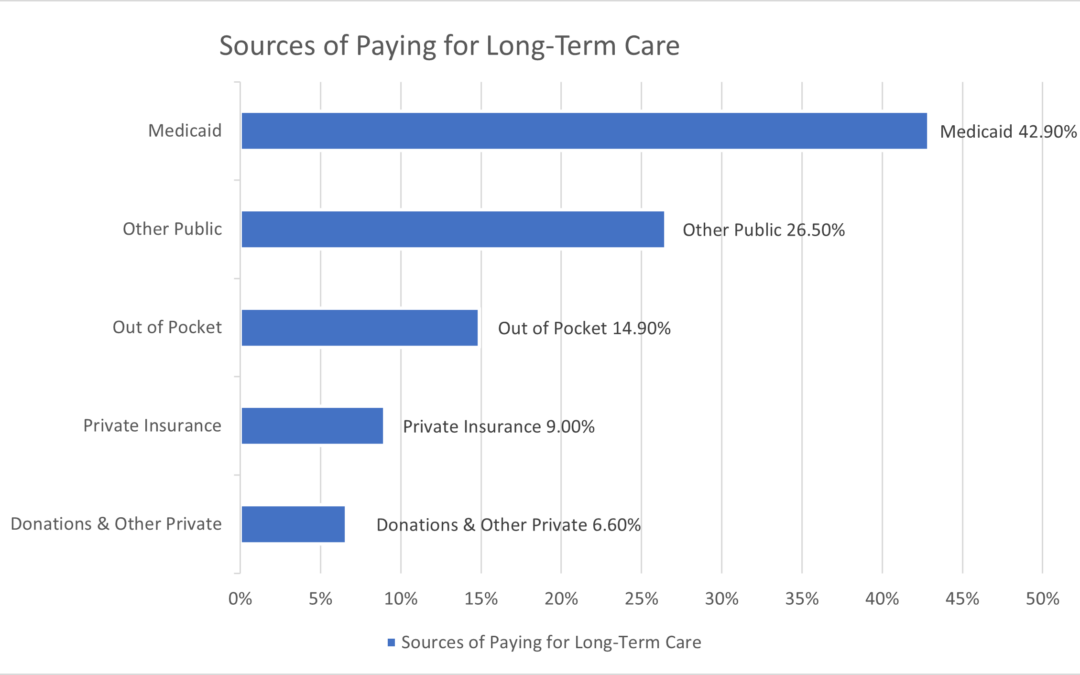

Sources of Paying for Long-Term Care

Source Note: CRS analysis of National Health Expenditure Account (NHEA) data obtained from the Centers for Medicare & Medicaid Service, Office of the Actuary, prepared December 2020

Donations and Other Private [6.6%]

Whether through fundraising organizations or direct contributions, philanthropic support accounts for a small portion of long-term care expenditures. However, older adults cannot rely on donations to pay the entire nursing home bill and must turn to other private or public means to cover costs.

Private Insurance [9.0%]

Some private insurance programs offer long-term care support, but Long-Term Care Insurance (LTCI) is responsible for most of this coverage. LTCI policies can be customized to fit each situation, and benefits cover any type of facility. The key is older folks must purchase LTCI while they’re still healthy.

Out of Pocket [14.9%]

Many older adults are unprepared for a long-term care stay and end up paying the bill out of their own pocket. While this portion may be feasible for individuals with a high net worth, the unfortunate reality is many of them will deplete their entire life savings within one year of entering a nursing home.

Other Public [26.5%]

Medicare, Veterans Affairs (VA), and other public programs may cover a portion of a long-term care stay but only in specific situations and only for qualified individuals. Plus, these public funds are typically not enough to cover the entire bill, requiring many older people to find additional coverage. Other Public Limitations: This includes Medicare coverage for temporary post-acute care in a skilled nursing facility, which is one of the only instances where Medicare covers a long-term care stay.

2022 VA AID & ATTENDANCE

MONTHLY PENSION RATES

Single Veteran $2,050

Married Veteran $2,431

Surviving Spouse $1,318

Veteran Married to Veteran $3,253

Medicaid [42.9%]

Medicaid is the largest payer of long-term care. It covers the cost of an individual’s custodial care in a nursing home, including room and board, pharmacy, and incidentals. However, in order to qualify for benefits, applicants must meet certain financial and non-financial criteria.

54%

By 2029, 54% of seniors will not have enough financial resources to pay for long-term care. (Health Affairs)

Planning for long-term care can be confusing, and more older adults are seeking a professional they can trust to help navigate this stage of life.

BATTLING THE MISCONCEPTIONS OF MEDICAID VS MEDICARE

Unfortunately, many seniors believe Medicare pays for long-term care. In reality, it will only cover skilled nursing care in a rehabilitative setting after a qualifying hospital stay of at least three days, and the coverage is temporary. Medicare only offers full coverage for 20 days and partial coverage for 80 additional days, which only applies if the patient continues to qualify under the rehabilitative category during the 100-day benefit period.

Part A Skilled Nursing Facility Coinsurance

Days 1-20: $0 for each benefit period

Days 21-100: $194.50 (for 2022) coinsurance per day of each benefit period

Days 101 and beyond: all costs

2.3 Years

The average stay in a nursing home is 2.3 year

(Centers for Disease Control and Prevention)

2050

The number of Americans who require long-term care

will more than double by 2050.

(Centers for Medicare and Medicaid Services)

70%

Older adults turning 65 today have almost a

70% chance of needing some type of

Long-term care

(U.S. Department of Health and Human Services)

______________________

WHERE DO WE COME IN?

Whether you, your family or loved one need pre-planning or crisis planning, the multidisciplinary team of professionals at Lifescape Law & Development has a solution to protect you, your health, your family, your assets and provide financial relief for the long-term. We thrive on providing creative and prompt personal services and creating customized approaches to fulfill you and your family’s needs that work in tandem with the guidance of your other professional advisers. Let’s work together through this process.

Recent Comments